Table of Contents

Section 1: The New Operating Reality

Section 2: Customer Intelligence Becomes a Competitive Requirement

Section 3: Specialization Rewrites the Competitive Map

Section 4: Culture Becomes an Operating Advantage

Section 5: From Hustle to Data-Informed Operations

Section 6: AI as a Discipline Multiplier

Section 7: What This Means for Rental Leaders in 2026

Introduction

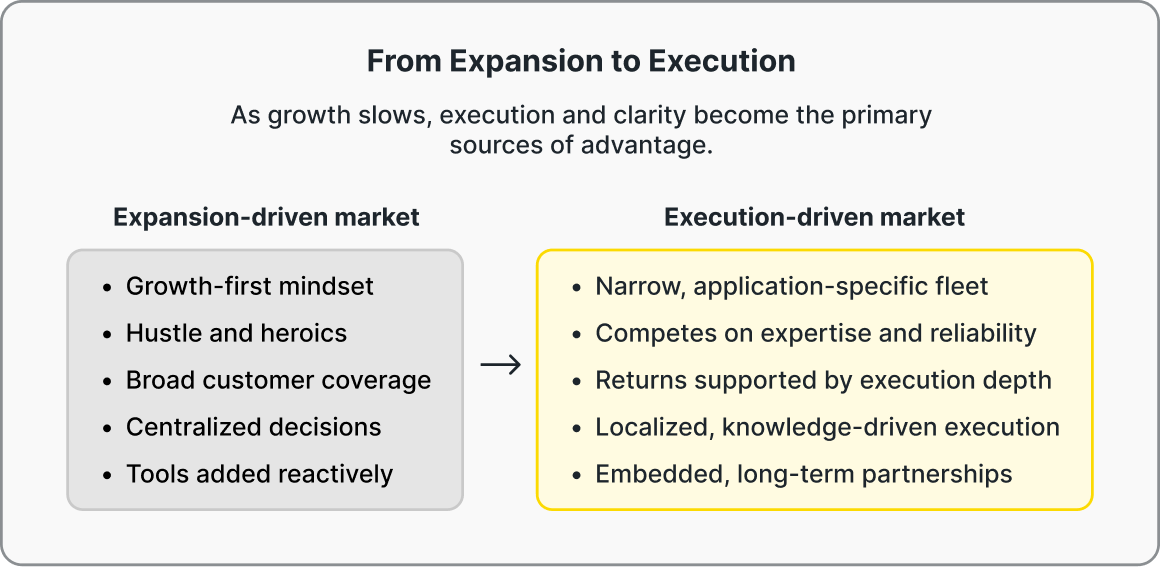

For much of the past decade, the equipment rental industry benefited from sustained demand, favorable capital conditions, and rapid expansion. Many rental businesses grew quickly, adding fleet, locations, and systems to keep pace with customer needs in a supply-constrained environment.

That environment is changing.

Industry forecasts point to a period of normalization. Growth is still present, but it is slower, less forgiving, and more dependent on execution than expansion. Inflation, interest rates, tariff uncertainty, and softer construction indicators are placing new pressure on rental businesses to operate with greater discipline and intention.

The industry is no longer debating whether technology, data, and process matter. Those questions have largely been settled. The challenge now is execution. In many cases, systems exist, but inconsistent usage, fragmented workflows, and manual coordination limit their impact on utilization, availability, and decision-making.

The findings in this report point to a clear theme. Performance gaps across rental businesses are widening, not because demand has disappeared, but because day-to-day operations have become harder to manage. As fleets, customers, and workloads grow, many operators lack consistent visibility into utilization, customer activity, and asset availability. Utilization remains uneven, customer value is concentrated, and maintenance and scheduling discipline varies widely. In this environment, averages can be misleading, masking wide differences in execution and making the typical operator’s experience harder to see.

This report examines how rental leaders are responding to the shift from growth-driven expansion to execution-driven operations. It explores how customer focus, specialization, culture, data discipline, and emerging technologies like AI are shaping the next phase of the rental cycle. The conversations reflect an industry that remains fundamentally strong, but increasingly aware that success in the years ahead will be defined less by growth at all costs and more by execution with intent.

This report draws on insights from more than 50 Rental Roundtable podcast interviews, a survey of over 35 independent rental operators, and anonymized platform data from Quipli customers across 2024 and 2025. It is further informed by industry forecasts, public company disclosures, and peer and partner research from organizations including the American Rental Association, S&P Global, and international rental publications.

Section 1: The New Operating Reality

Uncertainty Without Contraction

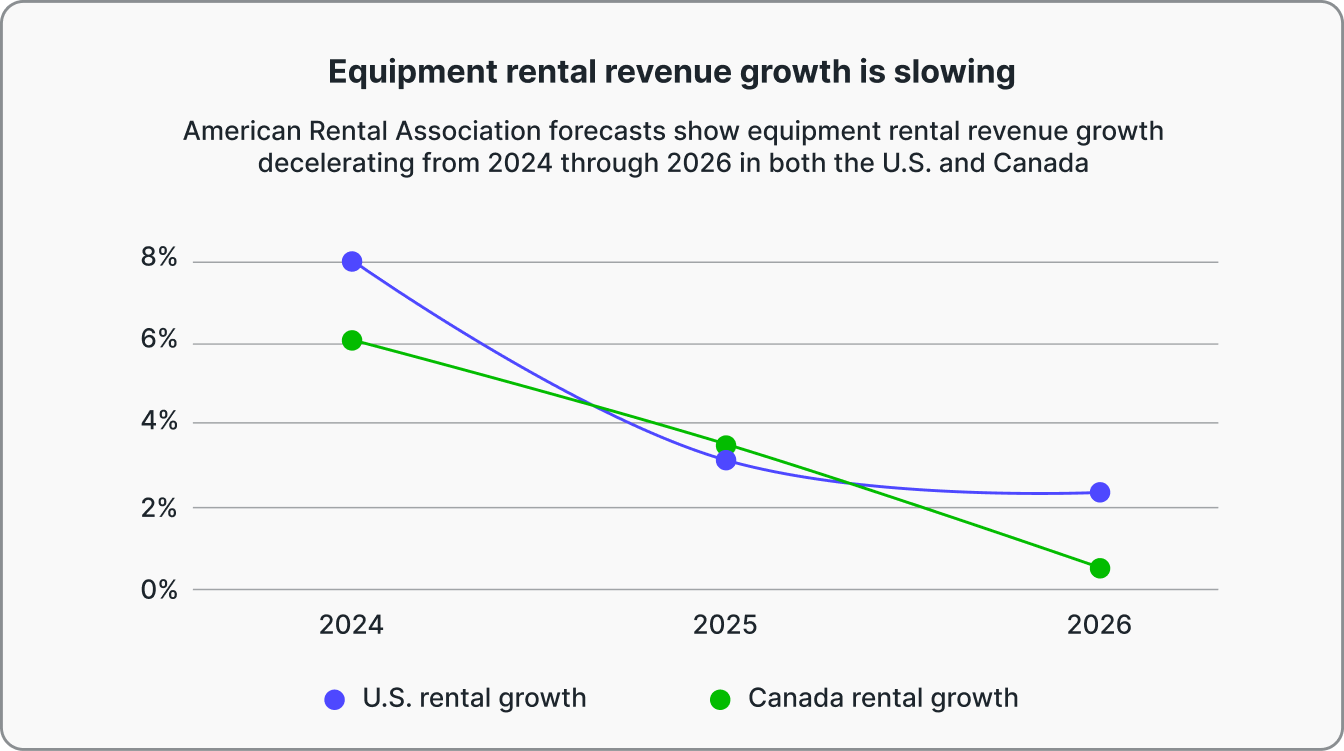

Industry-wide forecasts reinforce that the equipment rental sector is entering a more disciplined phase of growth.

In its November 2025 outlook, the American Rental Association projected U.S. construction and general tool rental revenue growth slowing to 3.3 percent in 2025, totaling $80.5 billion, followed by further deceleration to 2.3 percent growth in 2026, reaching $82.3 billion. In Canada, the slowdown appears even more pronounced, with rental revenue expected to grow 3.5 percent in 2025 to $5.9 billion, before dropping to just 0.6 percent growth in 2026.

Construction and industrial equipment remains the industry’s primary demand driver, accounting for approximately $63.4 billion of U.S. rental revenue in 2025, compared with $17.1 billion from general tool rental. As a result, rental performance remains closely tied to construction activity and infrastructure investment, with ARA framing 2026 as a year to “hold your own and prepare for better days to come.”

Importantly, this outlook reflects uncertainty rather than contraction. Scott Hazelton, consulting director at S&P Global, emphasized that the defining challenge is not a sudden loss of demand, but the prolonged duration of policy uncertainty. Tariff negotiations, shifting trade assumptions, and an extended government shutdown limited the availability of new construction data late into 2025, complicating forecasting and weighing on business confidence.

Historically, periods of heightened uncertainty have tended to support rental demand rather than undermine it. Hazelton noted that rental penetration has increased during nearly every episode of elevated uncertainty that was not accompanied by recession, as contractors delay capital purchases and opt to rent instead.

Capital Becomes More Discerning

These forecasts align with how experienced industry participants describe the current phase of the cycle.

From a capital and consolidation perspective, Dan Conway, managing partner at Craft Partners, an investment banking firm that specializes exclusively in mergers and acquisitions within the equipment rental industry, described a clear shift in transaction activity beginning in 2024. After completing six transactions in 2022 and a similar number in 2023, Conway observed a noticeable slowdown in mergers and acquisitions starting around March 2024. He linked this change to rising interest rates, noting that higher borrowing costs disproportionately impact middle-market buyers and reduce deal volume.

Conway also observed that major national rental companies became more selective in their acquisition strategies during this period. While consolidation has not stopped, buyers have pulled back on the number of transactions they pursue, focusing instead on fewer, more strategic opportunities. At the same time, Conway pointed to recent high-profile acquisitions, including competing bids by United Rentals and Herc for H&E, as evidence that large players remain bullish on the long-term prospects of the industry, even as near-term conditions require greater scrutiny and patience.

Supply Normalization and Inventory Pressure

On the supply side, Clement Cazalot, co-founder and CEO of Machinery Partner, a B2B marketplace and technology platform for heavy industrial equipment, described visible signs of normalization based on firsthand market observations. At a recent Ritchie Bros. auction, Cazalot noted record-breaking volumes of equipment on the ground, describing it as one of the largest auctions he had seen in terms of asset count. What stood out most was the presence of brand-new equipment at auction, including entire rows of new mini-excavators, attachments, and dirt-moving equipment. He emphasized that this was unusual and suggested it reflected a market carrying more inventory than it could immediately absorb.

Cazalot also observed that manufacturer order books were lighter compared to the previous one to two years, indicating that supply chains which had previously been constrained were now well stocked. He pointed to the growing presence of new and near-new equipment at auction as a signal of over-fleeting and, in some cases, financial stress, including repossessions and efforts by companies to reduce leverage. Taken together, these signals suggested softer pricing pressure and a market adjusting after a period of rapid expansion.

Strong Revenue, Tighter Margins

Public market results reflect a market that remains active but increasingly operationally demanding. United Rentals reported record third-quarter 2025 rental revenue and raised its full-year revenue and capital spending guidance, citing continued customer demand. At the same time, management noted ongoing cost pressures and normalization in certain areas of the business, including used-equipment sales, which weighed on margins. The results underscore that even at scale, strong revenue performance does not automatically translate into margin expansion, placing greater emphasis on operational efficiency and cost discipline to sustain performance.

Viewed alongside the ARA forecast, these perspectives point to the same conclusion. The rental industry remains fundamentally healthy, but the margin for inefficiency is narrowing. Capital is more selective, inventory is more visible, and growth is no longer sufficient to mask operational weaknesses.

In this environment, how rental companies operate matters more than how quickly they expand. The leaders featured throughout this report consistently describe a shift away from growth at all costs toward clearer priorities around customers, processes, people, and decision-making. The sections that follow examine how those priorities are taking shape across the industry.

Section 2: Customer Intelligence Becomes a Competitive Requirement

As rental markets mature and growth moderates, advantage is shifting away from broad customer coverage toward deeper understanding of the customers that matter most. Across interviews, survey responses, and platform data, operators consistently described a move away from treating all customers equally and toward intentionally prioritizing a smaller set of high-impact relationships.

Customer Activity Is Uneven by Design

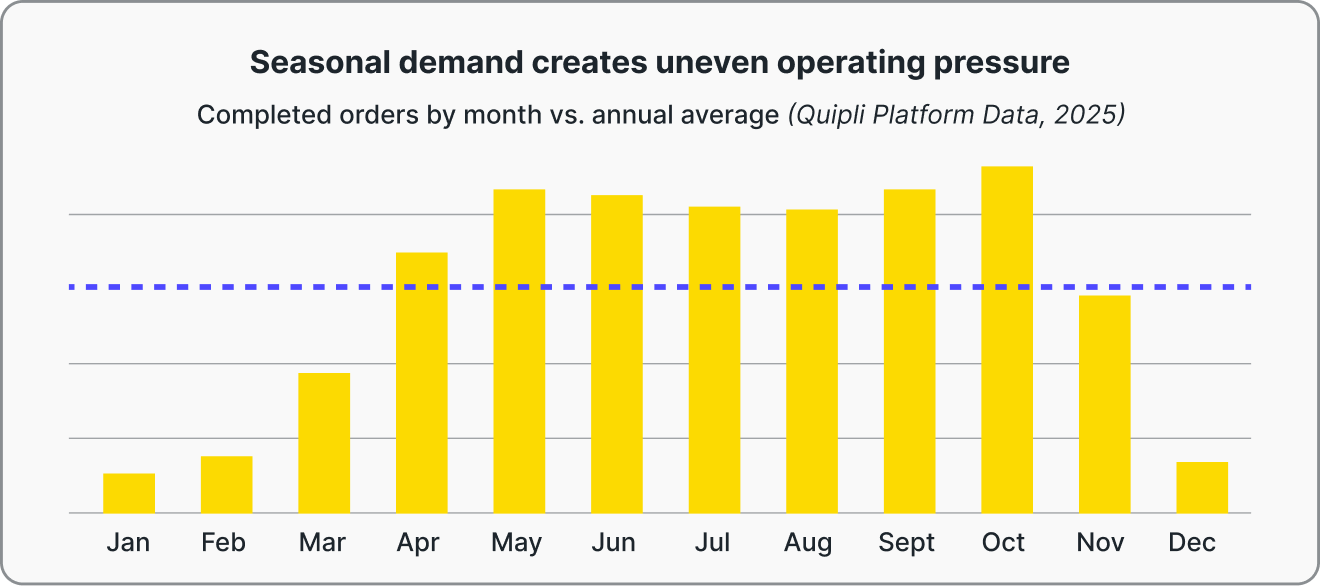

Seasonality is a defining feature of the equipment rental industry, with warmer months consistently driving higher levels of demand. Construction schedules, weather conditions, and project timing naturally concentrate rental activity into a predictable portion of the year.

However, seasonality alone does not explain how rental demand shows up in daily operations. Data from Quipli’s platform shows that completed orders fluctuate sharply month to month, even within the peak season itself. Periods of concentrated demand are often followed by abrupt slowdowns, creating swings that are large relative to average activity. When staffing, fleet availability, and service levels are planned around steady demand or headline averages, these fluctuations create avoidable strain.

In practice, operational pressure does not rise and fall smoothly. It arrives in clusters, stretching dispatch, maintenance, and availability at the same time. The implication is not to overreact to every spike or lull, but to recognize that time, flexibility, and operational attention must be allocated deliberately. As growth slows, the cost of misalignment becomes harder to absorb.

From Awareness to Strategy

Survey responses from more than 35 independent rental operators reinforce a clear gap between awareness and execution. When asked whether they actively analyze which customers drive most of their revenue, 45.9 percent of respondents said they do so regularly, 48.6 percent said they do so only occasionally, and 5.4 percent said they do not analyze customer concentration at all.

In practice, this means that while nearly all operators recognize that customer value is uneven, fewer than half have made it a consistent operating discipline.

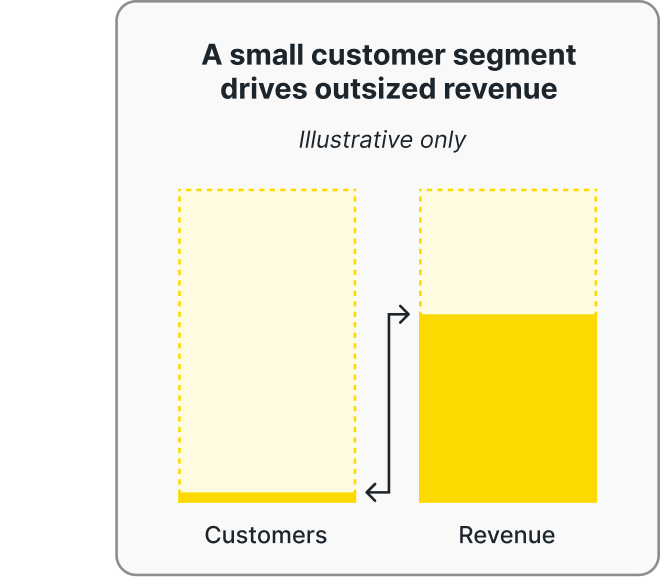

Nick Mavrick, CEO and founder of BiltData.ai and a former executive at NationsRent and Volvo Rents, provided one of the clearest illustrations of how concentrated customer value is in rental operations. Drawing on internal data from his time at NationsRent, Mavrick noted that approximately 3 percent of customers drove more than 60 percent of total revenue, with the top 11 percent accounting for more than 80 percent.

This level of concentration was not an anomaly, but a repeatable pattern observed across locations and business units. Based on this pattern, he argued that independent rental companies should avoid competing broadly with national chains and instead design their businesses around a small set of high-impact relationships.

In practice, he advised identifying 15 to 30 priority customers per location and aligning capital, service levels, and sales effort around serving those accounts exceptionally well. Mavrick emphasized that this approach allows independents to compete where scale is weakest, by delivering personalized, flexible service and planning fleet and investment decisions around customer needs rather than available inventory. As Mavrick stated: “Marketing is not magic, it’s math. You can pick your customers before they pick you and beat the competition.”

Mavrick also highlighted the importance of understanding a customer’s share of wallet, not just individual transactions. By knowing how much a customer rents overall, operators can price competitively on high-frequency items while capturing stronger margins on less common rentals, reinforcing both loyalty and profitability.

Customers Are Asking for More Than Equipment

From the renter’s perspective, deeper engagement matters. Dan Maitland, fleet manager at Ajax Paving and a former rental operator, described how the most valuable rental partners move beyond transactional fulfillment. He emphasized the importance of proactive communication, particularly around upcoming work and equipment needs, and highlighted quarterly business reviews as a practical way rental companies can use usage data to help customers make better rent-versus-own decisions. Maitland noted that rental providers who understand how equipment is actually used on the jobsite and proactively flag issues or opportunities are more likely to earn trust and long-term relationships.

A longer-term perspective emerged from Joe Kondrup, a co-founder of United Rentals and the founder of Catalyst Strategic Advisors, alongside Josh Mosko of Catalyst. Drawing on their experience building and advising large and specialty rental businesses, they noted that customers increasingly prefer working with fewer rental partners who can support complex, multi-category needs. As rental offerings become more specialized and engineered, customers prefer working with fewer partners who understand their operations and can support multiple needs reliably.

This shift moves rental relationships away from transactional fulfillment and toward application-specific support. In practice, this means customers expect rental providers to understand how equipment is used on the jobsite, how different assets interact, and how operating conditions affect outcomes. Providing equipment alone is often no longer sufficient.

Focus Becomes a Competitive Advantage

Taken together, interviews, survey responses, and platform data point to the same conclusion. In a more disciplined market, customer focus is no longer optional.

The rental companies pulling ahead are not those with the largest customer lists, but those with the clearest understanding of who they are building for. They allocate resources deliberately, design fleets around real demand, and build operating models that reflect how customers actually behave.

Customer intelligence, in this context, is not just having access to data. It is the consistent use of that data to guide daily decisions.

Section 3: Specialization Rewrites the Competitive Map

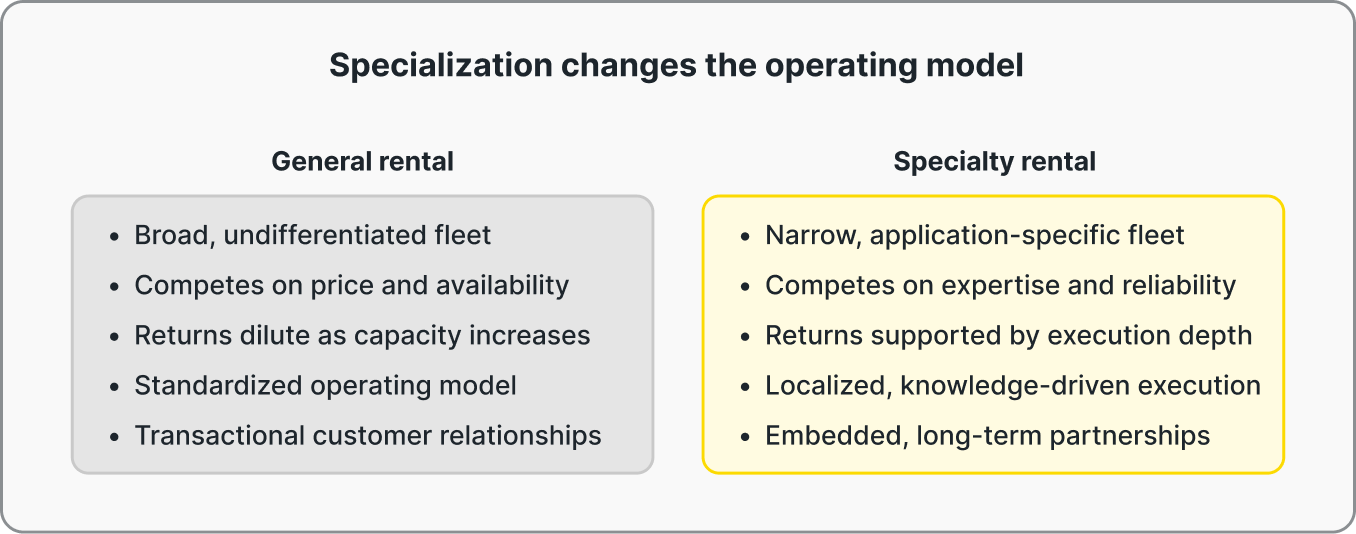

As customer intelligence sharpens and revenue concentration becomes unavoidable, many rental companies are arriving at the same conclusion: general rental alone is increasingly difficult to defend. Across interviews, operators and advisors described structural pressures that make specialization less of a growth tactic and more of a competitive necessity.

General rental faces structural limits

Joe Kondrup and Josh Mosko described general rental as increasingly constrained by both capacity and differentiation. At a market level, they noted that metropolitan areas can absorb only so much undifferentiated fleet before additional equipment begins to dilute rates rather than generate incremental profit. As general rental capacity increases, competition shifts toward price and availability, making it harder for additional fleet to earn acceptable returns.

Against that backdrop, Joe Kondrup and Josh Mosko pointed to specialization as a structural response rather than a tactical one. Mosko noted that at United Rentals, approximately 40 percent of the business is now driven by specialty equipment, reflecting a deliberate shift away from reliance on commodity rental alone.

“If you listen to United Rentals’ investor calls, about 40 percent of their business is now driven by specialty. That’s a massive number. It reflects the shift toward engineered, application-based solutions that create real value and minimize downtime.”

Rather than acting as supplemental capacity, specialty offerings allow rental providers to become embedded partners on complex projects. Mosko emphasized that this shift is driven as much by customer needs as by competitive pressure. Large infrastructure, data center, and industrial projects increasingly require engineered solutions that combine equipment, accessories, and technical support into complete systems rather than standalone rentals.

Meeting these requirements demands application knowledge, experienced personnel, and an understanding of how assets interact on the jobsite. In this environment, supplying general-purpose equipment alone is often insufficient, and differentiation comes from the ability to deliver reliable, integrated solutions.

Together, their perspective highlights the core limitation of general rental. As markets mature and fleets expand, adding more undifferentiated equipment becomes less effective. Value increasingly accrues to operators who can specialize, where technical depth and execution create defensible advantages that scale alone cannot provide.

Industry Data Confirms the Shift Toward Specialization

Industry data has reinforced this shift over the past several years. In a November 2024 article, the American Rental Association documented sustained growth in specialty rentals, citing strong year-over-year growth reported by major rental operators as customer needs become more segmented and application-specific. The article highlighted a range of specialty offerings, including climate control, power and infrastructure services, trench shoring and underground safety equipment, event support, and disaster response, illustrating how rental companies are building around narrow, application-specific use cases rather than general-purpose fleets.

The coverage described how specialty offerings, often delivered as bundled or engineered solutions, are increasingly positioned as core components of long-term growth strategies.

Why Specialization Changes the Operating Model

Clement Cazalot reinforced this dynamic from a structural perspective. He noted that while national rental companies excel at scale and standardization, they often struggle with the localized complexity and uneven utilization profiles associated with specialty equipment. As a result, large operators may avoid or exit categories that do not fit their operating model, creating opportunities for independent and regional rental companies with deep local expertise.

Cazalot highlighted that equipment requirements vary meaningfully by geography, geology, climate, and industry. What works efficiently in one region may not translate well to another. This localization limits the advantage of national scale and rewards operators with deep market knowledge. Independent rental companies are often better positioned to build expertise around narrow use cases, tailor fleet and service to local demand, and respond more flexibly than standardized platforms.

He also noted that while rental ownership continues to consolidate, the manufacturing landscape is fragmenting. New global OEMs and specialized manufacturers are entering the U.S. market, particularly as equipment technology evolves. This fragmentation creates additional access points for rental companies willing to specialize, even as general rental becomes more crowded.

A Disciplined Response to a Slower Market

Across interviews, specialization was not framed as a growth-at-all-costs strategy. Instead, it was described as a more disciplined way to deploy capital and focus operational effort in a slower, more competitive market. Cazalot emphasized the importance of aligning growth with operational capacity, particularly in an environment marked by higher inventory levels, softer pricing signals, and tighter capital conditions.

These perspectives point to a consistent pattern. As general rental faces increasing commoditization and pricing pressure, specialization offers a structurally different path forward. It reshapes customer relationships, alters operating requirements, and creates forms of differentiation that scale alone cannot provide.

In the sections that follow, this shift toward specialization intersects with culture, data discipline, and technology, highlighting how successful rental companies are building systems that support deeper expertise without sacrificing operational control.

Section 4: Culture Becomes an Operating Advantage

As rental companies grow more complex, culture has shifted from a soft concept to a structural one. Across interviews, leaders described culture not as a set of values, but as the system that determines how decisions are made, how quickly problems are resolved, and how consistently customers are served.

In a slower-growth environment, culture increasingly functions as an operating advantage.

Decision-Making Moves to the Edge

At City Rentals, decision-making authority is intentionally pushed to the front lines of the business. Eddie Wilson described an environment where counter staff, yard personnel, and delivery drivers are trusted to make high-stakes calls without prior approval.

Counter staff are empowered to refuse rentals when something feels off. Yard teams are expected to flag suspicious behavior. Delivery drivers are trusted to assess job sites and raise concerns if conditions appear unsafe or illegitimate. In each case, employees are supported by management even when their judgment proves overly cautious.

Wilson was explicit about the principle behind this approach: employees are never penalized for protecting the business. Removing fear from decision-making reinforces accountability and speeds response at the moment risk appears. Asset protection, in this model, is driven less by policy and more by trained judgment applied in real time.

Premier Truck Rental (PTR) applies a similar philosophy in a very different operating context. Chris Keys described how decision-making authority is distributed across integrated teams made up of territory managers, inside sales representatives, and rental coordinators. Each team owns its customer relationships and daily execution, with minimal micromanagement.

Rather than routing decisions through layers of approval, PTR emphasizes transparency, shared visibility, and clear goals. Employees are expected to make informed calls when issues arise, with leadership providing context rather than constant oversight.

Human Judgment Where Systems Fall Short

In both organizations, certain operational challenges are intentionally handled by people rather than software.

At City Rentals, theft prevention relies heavily on human intuition. Wilson emphasized that many losses are avoided through deliberate conversations at the counter, where employees take time to understand the job and assess inconsistencies. These interactions often last 10-15 minutes and are designed to surface risk before equipment ever leaves the yard.

At PTR, Keys described a similar reliance on judgment in customer relationships. Situations involving equipment damage, disputed charges, or custom configurations are approached as partnerships rather than strict contract enforcement. While agreements exist as guardrails, the first response is conversation, context, and problem-solving.

Where this judgment is absent, operational friction tends to surface in less visible ways. Quipli platform maintenance and downtime data surfaces cases where assets remain marked as unavailable for extended periods, even when active repair work is limited. Rather than indicating mechanical complexity, these situations highlight how availability hinges on clear ownership and timely follow-through. The insight reinforces a broader pattern: systems like Quipli make gaps visible, but performance improves when teams consistently act on what the system reveals.

Across these examples, culture directly shapes both risk exposure and response time. Organizations that push authority to the operational edge move faster, surface problems earlier, and avoid the bottlenecks that emerge when decisions are centralized. As complexity increases and staffing and system constraints persist, the ability to act quickly and consistently becomes a measurable operational advantage rather than a cultural ideal.

An Asset That Compounds Over Time

Unlike fleet or facilities, culture compounds. Strong cultures improve execution, reduce turnover, and create consistency across locations. Weak cultures amplify complexity and slow decision-making as organizations grow.

The leaders featured in this section treated culture as something to be designed and reinforced deliberately. In a market where efficiency matters more than expansion, that intentionality is becoming a meaningful differentiator.

As rental companies navigate the next phase of the cycle, culture increasingly determines who can scale with discipline and who struggles under the weight of their own complexity.

Section 5: From Hustle to Data-Informed Operations

For many independent rental companies, early success is built on hustle. Owners answer every phone call, manage dispatch themselves, and rely on experience to make fleet and pricing decisions. In the early stages, this approach works.

But across interviews and data, a consistent pattern emerges: what drives growth early eventually becomes the constraint that limits it.

As rental businesses scale, complexity increases faster than visibility. More equipment, more customers, and more jobs introduce coordination challenges that effort alone cannot solve. Operators described hitting a point where they were no longer constrained by demand, but by their ability to manage information, workflows, and decisions across the business.

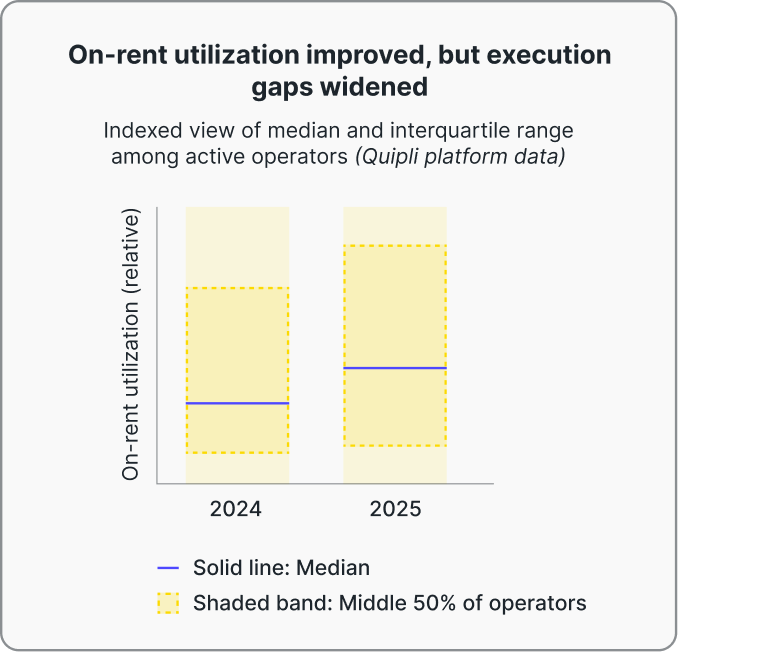

Utilization Exposes the Execution Gap

Quipli’s anonymized platform utilization data reinforces this shift. Overall on-rent percentages improved modestly from 2024 to 2025, with both median and upper-quartile utilization increasing year over year. At the same time, performance dispersion widened, with the interquartile range expanding from 7.6 to 10.6 percentage points, highlighting growing differences in execution across operators.

Category-level utilization data from the Quipli platform adds further clarity. Physical utilization concentrates in a narrow set of core categories, particularly compact earthmoving and access equipment, while many other categories turn far more sporadically. These core categories account for a disproportionate share of fleet activity, while the remainder of the fleet experiences longer idle periods.

As businesses grow, unmanaged concentration increases risk. When utilization becomes heavily dependent on a small number of categories without corresponding alignment in dispatch, maintenance, availability, and pricing, breakdowns in any one area can cascade across the operation.

Maintenance Data Highlights Why Medians Matter

Maintenance and downtime data reinforces the same theme from a different angle. Asset availability varies widely across fleets, with some units experiencing extended periods of downtime that are not directly tied to the complexity of the repair itself.

In many cases, prolonged unavailability reflects coordination factors such as parts lead times, scheduling gaps, inspection timing, or delayed handoffs between teams. When these factors are not visible, availability constraints can appear structural even when capacity exists, making it harder to identify where intervention will have the greatest impact.

The Internal Breaking Point

Haymond Meinhardt’s experience at Brandywine Rentals illustrates how growth driven by hustle can eventually strain visibility and coordination. As the company expanded from a small, family-run operation into a business with roughly 40 employees operating out of a single location, Meinhardt remained deeply involved in sales, dispatch, and day-to-day problem solving, often handling 60 to 80 calls per day.

This approach worked during earlier stages of growth, particularly when fleet expansion was driven directly by daily customer feedback rather than formal analysis. Over time, however, the concentration of operational knowledge in one person became a limiting factor. Eventually, Brandywine hired a dedicated dispatcher, marking a shift away from ad hoc coordination toward clearer role definition and workflow separation.

The change did not reflect a slowdown in demand, but the need to reduce dependence on individual memory and constant intervention as activity increased. Meinhardt’s experience highlights a common transition point in growing rental businesses: sustained growth requires moving operational knowledge out of individuals and into shared processes that can support clearer visibility and more consistent execution.

From Intuition to Visibility

Luke Powers, founder and CEO of Gearflow and a former rental operator, reinforced the same execution constraint from the contractor’s side of the market. He emphasized that equipment uptime is not an abstract metric, but a direct economic driver on the jobsite. In one contractor study he referenced, a paver going down was estimated to cost $234 per minute, or more than $100,000 per day, underscoring how quickly coordination failures translate into real financial impact. Even smaller assets, he noted, carry a measurable cost when they are unavailable.

Powers connected these uptime pressures to how work is actually coordinated today. He described procurement and logistics workflows as largely manual, relying on phone calls, emails, texts, and spreadsheets rather than structured systems. In that environment, availability problems are often less about mechanical failure and more about delayed communication, missed handoffs, or lack of shared visibility across teams.

He also highlighted a growing labor constraint, noting that experienced workers are leaving the industry faster than new entrants are arriving. As institutional knowledge thins, reliance on individual memory and ad hoc coordination becomes riskier. His perspective reinforces the core pattern in this section: as complexity increases and human capacity tightens, visibility and disciplined workflows shift from being helpful to being essential.

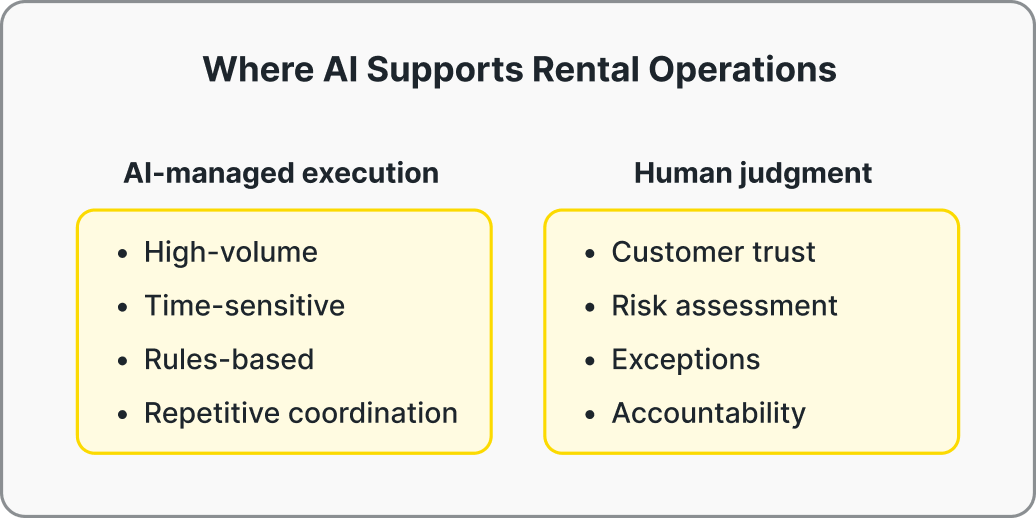

Section 6: AI as a Discipline Multiplier

As rental businesses move into a slower, more execution-driven phase of the cycle, artificial intelligence is no longer being discussed as a future concept. Across interviews, it emerged as a practical response to a familiar constraint: the growing gap between operational complexity and human capacity.

Importantly, AI was not framed as a replacement for people or relationships. Instead, operators and technologists described it as a way to reinforce discipline, consistency, and speed in parts of the business where manual execution breaks down under volume.

Where AI Is Showing Up First

The clearest AI use cases discussed across interviews were not abstract or experimental. They were concentrated in high-volume, time-sensitive workflows where responsiveness directly affects revenue and customer experience.

Jesse Buckingham, founder of Vooma, a platform that enables logistics companies to build and manage AI agents for transaction-heavy operations, described this dynamic through his work in freight brokerage. He argued that the most useful way to think about AI in equipment rental is not as a new tool, but as automation applied to familiar workflow patterns. Drawing on his experience across freight and rental-adjacent operations, he described a common operational reality: work often happens when someone manually moves information from one system to another. He emphasized that this pattern is not unique to logistics and expects AI adoption to spread broadly across industries, including rental.

From his perspective, one of the earliest rental applications is a more continuous customer experience. He predicted that rental customers will increasingly be able to interact with AI 24/7 to get questions answered, with the AI connected to core business systems so it can understand pricing, inventory, and operational details. He also pointed to back-office processes as a high-likelihood area for AI agents, specifically highlighting invoicing, billing details, and reconciliations as workflows that could shift from manual coordination to agent-driven execution.

Buckingham framed the longer-term operating model shift as integration. As agents become embedded into business systems, the role of people moves away from repetitive data transfer and toward overseeing automated workers, managing exceptions, and ensuring execution stays aligned with business rules.

From Workflow Automation to Real-Time Execution

Scott Cannon, CEO of BigRentz, a national rental procurement platform that connects construction contractors with thousands of independent rental companies across the U.S., described how AI is being applied to reduce execution friction in rental workflows at scale.

At BigRentz, AI is used to support pricing, availability, and logistics decisions across a large volume of rental transactions. Cannon explained that these decisions are trained on historical rental contracts and prior sourcing outcomes, allowing pricing and fulfillment decisions that once required manual coordination to be executed in real time. In practice, this reduces latency between customer intent and equipment delivery, particularly on time-sensitive construction projects.

Cannon emphasized that this automation does not replace people. Instead, it removes manual system-to-system coordination in workflows where delays compound quickly. In construction, where missed deliveries or inaccurate assumptions can immediately erode project profitability, the value of AI lies in consistency and speed rather than judgment or relationship management.

Across both interviews, the common theme was consistent. AI delivers value where work is repetitive, time-sensitive, rules-based, and dependent on fast response. These are precisely the areas where human execution tends to degrade as volume increases.

What AI Does Not Replace

Across interviews, there was clear alignment on AI’s limits. While automation improves speed and consistency, it does not replace accountability, judgment, or trust in customer relationships.

Luke Powers, speaking from the contractor’s perspective, underscored that responsiveness matters because downtime carries immediate financial consequences, but reliability ultimately depends on confidence in the rental partner. When issues arise, such as missed deliveries, equipment problems, jobsite constraints, customers value clear ownership and informed decision-making over automated responses.

Rental operators echoed this boundary. Tasks such as customer qualification, risk assessment, dispute resolution, and exception handling continue to rely on human judgment. In this context, AI’s role is not to remove people from the process, but to reduce the coordination burden around them, allowing teams to focus attention where experience and context matter most.

Applying AI to Revenue Execution

From Quipli’s perspective, the most immediate opportunity for AI in rental is revenue execution.

Quinn is Quipli’s AI platform designed to address this gap by operating continuously across front-end rental workflows. It monitors calls, messages, and customer activity for revenue signals such as new inquiries, changes in rental behavior, or upcoming work, and surfaces those signals to sales teams in real time.

Rather than functioning as a reporting or analysis tool, Quinn is designed to automate follow-up and prioritization, helping ensure that opportunities are captured consistently, including outside normal business hours or during periods of high volume.

In the context of a slower, more execution-driven market, Quinn reflects how AI is being applied in rental: not to replace judgment, but to reinforce consistency in revenue-critical workflows where human execution tends to break down under load.

Readiness Matters More Than Tools

Across interviews, a consistent caution emerged. AI amplifies whatever operating discipline already exists. Operators emphasized that meaningful value depends on having clear workflows, reliable data, and defined ownership in place first. Without those foundations, automation tends to accelerate confusion. With them, AI increases speed and consistency without displacing human judgment.

These perspectives point to a more grounded phase of AI adoption in rental. AI is increasingly treated as an operational capability, not a strategic identity. Its value lies in reinforcing execution where volume and responsiveness matter most. In this environment, advantage accrues to companies that apply AI deliberately within disciplined operations, not those chasing tools in place of fundamentals.

Section 7: What This Means for Rental Leaders in 2026

Across interviews, survey responses, and platform data, one conclusion consistently emerged. The defining challenge for rental leaders in 2026 is not a lack of opportunity, but a narrowing margin for error.

Growth has not disappeared, but it has become more selective. Capital is more expensive. Customers are more demanding. Operational gaps surface faster and cost more when they do. In this environment, success is shaped less by expansion and more by execution.

Discipline Is No Longer Optional

Many of the operators featured in this report described moments where the behaviors that once fueled growth began to limit it. Hustle turned into overload. Informal processes broke under volume. Centralized decision-making slowed response times just as expectations increased.

The implication for rental leaders is straightforward. Discipline is no longer something to layer in later. It is now a prerequisite for sustainable performance. Companies that lack clarity around who their best customers are, which assets truly perform, and how decisions are made tend to feel pressure everywhere at once. Those that establish this clarity gain room to operate, even in slower markets.

Focus Becomes a Competitive Advantage

Another consistent signal across interviews was a narrowing of strategic focus.

Rather than trying to serve every customer and category equally, successful operators are becoming more deliberate about where they invest time, fleet, and attention. For some, this means prioritizing a smaller group of high-impact customers. For others, it means specializing in categories where expertise and application knowledge matter more than sheer availability.

In each case, the underlying shift is the same. Optionality has become expensive. Attempting to be everything to everyone increasingly dilutes pricing, execution, and culture simultaneously. Focus, by contrast, allows rental businesses to align their operating models with real demand and build relationships that are more durable over time.

People Remain the Constraint

Despite growing interest in automation and technology, the report surfaced a less comfortable truth. People remain the primary constraint in rental operations.

Growth slows not because demand disappears, but because organizations struggle to delegate effectively, trust teams with real authority, and maintain clarity as they scale. Where decision-making remains centralized or ambiguous, complexity compounds quickly. Where trust, ownership, and accountability are designed intentionally, operations scale more smoothly.

Technology can support this shift, but it does not resolve it on its own. Leadership remains the determining factor.

Technology Rewards Readiness

Throughout the report, technology consistently appeared as an amplifier rather than a solution.

Data, automation, and AI create leverage only when foundational discipline is already in place. Clear workflows, reliable data, and defined ownership determine whether technology reduces friction or introduces more noise. In many cases, the most valuable step forward is not adding another tool, but simplifying and clarifying what already exists.

For rental leaders, this reframes the question. The challenge is not whether to adopt new technology, but whether the organization is ready to use it well.

A Different Kind of Leadership

Taken together, these signals point to a quieter but more demanding form of leadership.

Rental leaders entering 2026 are being asked to make fewer, better decisions, build organizations that function without constant intervention, and choose discipline over speed when the two conflict. This work is less visible than rapid expansion, but it compounds over time.

The companies that emerge strongest from this phase will not be those that moved fastest, but those that built with intention. In a market where execution matters more than growth, clarity becomes the most durable advantage.

Appendix

This report draws on qualitative insights, survey responses, and anonymized operational data to reflect current conditions and emerging patterns across the equipment rental industry. Sources include the following:

Industry Research and Public Sources

- American Rental Association (ARA): Q4 Economic Forecast for U.S. and Canada

- American Rental Association (ARA): Equipment Rental Industry Expected to See Softening Growth

- American Rental Association (ARA): Specialty rentals on the rise: Catering to unique consumer needs

- United Rentals: United Rentals Announces Strong Third Quarter 2025 Results and Raises Full-Year Guidance for Revenue and Capital Spending Supported by Strong Customer Demand

Rental Roundtable Interviews

Insights throughout the report are informed by more than 50 Rental Roundtable interviews conducted in 2025. Interviewees include independent rental operators, executives from national rental companies, contractors, industry advisors, and technology providers. Individual perspectives are attributed in the report where referenced.

State of Rental Survey (2026)

The report incorporates findings from a 2026 State of Rental survey completed by more than 35 independent rental operators across North America.

Quipli Platform Data

Select sections of the report reference anonymized, aggregated data from Quipli’s rental management platform, covering activity across 2024 and 2025. Platform data includes booking activity, physical utilization, and maintenance and downtime patterns.